CLMV economy is poised for a more robust growth in 2022 compared to 2021, backed by an easing of COVID-19 restrictions, higher regional vaccination rates which prompt border reopenings, and buoyant exports. Based on EIC estimation, GDP in 2022 will record a 4.8% growth for Cambodia, 4.0% for Lao PDR, 0.5% for Myanmar, and 6.5% for Vietnam.

Despite tailwinds from exports that regained momentum in line with the global economy, the CLMV economy still witnessed only a modest recovery throughout 2021, dragged by Delta outbreaks in Q2 and Q3?the most severe pandemic waves so far, which prompted the government to retighten lockdown rules. Meanwhile, the Myanmar military coup in February 2021 has resulted in a large economic contraction and aggravated pandemic impacts. Nonetheless, the CLMV economy showed signs of recovery in Q4 as the number of new infections decreased (to hundreds per day in CLM, except for Vietnam). Other forces behind an economic rebound came from higher vaccination rates (as of March 2, 2022, the fully-vaccinated accounted for 81.8% of the population in Cambodia, 58.7% in Lao PDR, 38.4% in Myanmar, and 78.5% in Vietnam), broad lifting of lockdown as the government shifted its strategy to living with COVID-19, and exports which returned with a strong growth after supply chain disruption gradually tailed off. Furthermore, Cambodia and Vietnam have started to reopen to foreign tourists by offering no or reduced period of quarantine for fully-vaccinated visitors. In our view, CLMV governments will likely ease the COVID-19 containment measures in 2022, which will help bolster domestic demand. Meanwhile, external demand should gain impetus from an improving global economy and border reopening to foreign visitors.

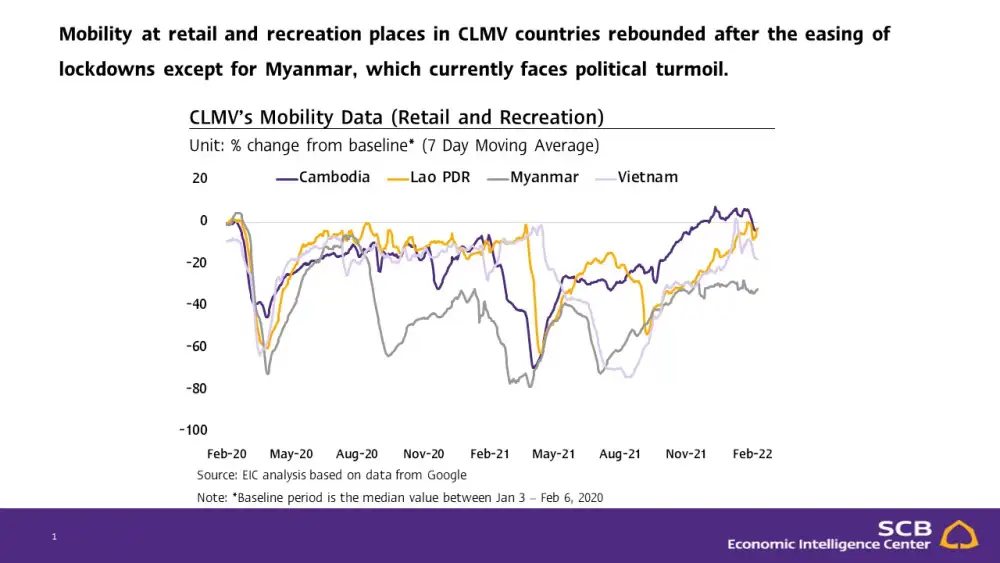

Domestic demand in CLMV economies should see a steady rebound in tandem with lockdown lifts and government stimulus, albeit facing pressures from economic scars and country-specific risks. Google Mobility data?which depicts movement trends across different places?showed a rebound in Retail and Recreation inall countries except Myanmar, reflecting a resumption in economic activities. Furthermore, CLMV employment is expected to regain footing, following an upswing in various economic sectors, particularly services. Most recently, Vietnam's jobless rate plummeted to 3.6% in Q4/2021 from 4.0% in Q3?such improved figure will likely drive domestic spending. Also, as Thailand started to hire more migrant workers, the remittance income among CLMV economies is poised to increase. Still, the pace of domestic demand recovery will be uneven, depending on fiscal strength and situation in each country. EIC expects Cambodia and Vietnam to have ample fiscal space for extra stimulus. Cambodia recently extended its financial reliefs for households to September 2022 while Vietnam announced economic stimulus worth 4% of GDP to be disbursed in 2022-2023. On the contrary, Lao PDR and Myanmar are confronted with fiscal constraints, thus unable to roll out sufficient supports to shore up the flagging economies. In particular, Myanmar will witness the slowest growth among peers as the political crisis prevails alongside sanctions imposed by western countries. Nevertheless, economic scars from the pandemic remain significant downside risks to domestic spending recovery. These headwinds include a swelling household debt and unemployment rate, which hung above its pre-pandemic level. The jobless figure may onlydecline slowly since some workers have pivoted to jobs in other economic sectors during the outbreaks.

On the external front, CLMV exports are expected to see a decelerating growth in 2022, whereas border trade and foreign direct investment (FDI) will gain impetus from border reopening. An easing of supply chain disruption and the opening of new border checkpoints will provide thrust to exports this year. Demand for CLMV products will continue its growth streak in line with global economic recovery and buoyant demand for 'New Normal' products, such as electronics and electrical appliances. In particular, Vietnam?as a production base of multinational electronics enterprises?will benefit most from such demand, as evident in a 19.0%YOY export growth in Q4/2021. Another impetus for CLMV exports is the Regional Comprehensive Economic Partnership (RCEP), which took effect from January 2022 and helps lift trade and investment barriers between CLMV and trade partners. Nonetheless, overall export growth in 2022 will see a deceleration from 2021 due to a higher base. Also, there remain downside risks and uncertainties from Omicron and new variant outbreaks that could evoke another supply chain disruption. Similarly, FDI will witness a steady rebound following a firm recovery among major regional economies and no-quarantine reopening to foreign visitors. RCEP would also help bolster investment into CLMV, particularly investment in businesses related to China-backed infrastructure projects under the Belt and Road Initiative in Cambodia, Laos and Myanmar?such as the China-Laos railway (Vientiane-Boten), which officially began service in December 2021. Meanwhile, Vietnam has been attracting foreign investors with key advantages: namely, a strategic location with short proximity to China, a large pool of young workforces, and extensive free-trade agreement coverage. CLMV governments may also consider more incentives to draw foreign investors. Cambodia enforced the New Investment Law in 2021 to reduce investment barriers, while Vietnam launched new tax incentives as a part of the recent economic stimulus. In contrast, Myanmar's exports and FDI rebound would be constrained by disruption in various economic sectors and worsening investor sentiment due to international sanctions and reputational risks.

Tourist arrivals to CLMV should pick up gradually in 2022, but the rebound would become more evident in the second half. In H1/2022, EIC expects foreign tourist arrivals to remain bleak on the back of the Omicron pandemic and mandatory quarantine. Fully-vaccinated foreign visitors are still subject to a 3-day quarantine on arrival in Vietnam, while Lao PDR restricts international arrivals only to group tours. Nonetheless, these strict measures should eased off in the second half as vaccination rates make headway while ebbing concerns over the Omicron variant would help bolster tourists to the CLMV region. Among CLMV countries, Cambodia was the first to welcome foreign tourists quarantine-free starting in November 2021 while Vietnam is expected to start welcoming foreign tourists in Mid-March, albeit with a one day quarantine and mandatory testing. Despite a sign of recovery, tourist arrivals will likely remain far below a pre-pandemic level, especially visitors from China, the largest part of the CLMV tourism sector, since the Chinese government is unlikely to lift its prohibition on international travel in 2022.

For the CLMV economy in 2022, key risks that warrant monitoring are 1) High uncertainties over Omicron and new variants outbreak, 2) Relatively low vaccination rates in Lao PDR and Myanmar, 3) Slower-than-expected global economic recovery amid rising geopolitical tensions, especially in China which has strong economic linkages with CLMV, 4) High energy prices due to the war between Russia and Ukraine which may lead to higher inflation and lower consumer purchasing power especially as CLMV currencies depreciate, and 5) Fiscal and monetary stability in the face of tightening global financial condition this year, particularly in Lao PDR and Myanmar where public debt is high relative to public revenue collection. Furthermore, there are some country-specific factors shaping economic prospects such as the prolonged political unrest in Myanmar which would continue to depress economic growth in all sectors.

Looking ahead, the CLMV economic recovery will benefit the Thai economy through higher exports and enhanced business opportunitiesin neighboring countries. Robust exports from Thailand to CLMV economies will likely continue, albeit at a slower pace. For Thai businesses, there are new opportunities for exporting agricultural products to China via China-Laos high-speed railway?an alternative that could significantly cut costs and transportation time. Moreover, Thailand's Commerce Ministry plans to open 12 new border checkpoints this year, but the plan might be put off if the COVID-19 infections resurge. Meanwhile, Thailand's outward FDI to CLMV will witness a modest rebound in line with the regional economy and no-quarantine reopening to foreign visitors. Vietnam is expected to maintain its position as the largest destination of Thai FDI among CLMV peers, whereas investment in Myanmar has fallen into severe stagnation due to political unrest. CLMV tourist arrivals in Thailand will likely improve in the second half after the Omicron pandemic subsides. Also, if Thailand reaches an agreement for 'Travel Bubbles' with CLMV countries, the arrangement would boost the plundered tourism sector, primarily through visitors across borders. Nevertheless, the high cost of COVID-19 testing and travel insurance might weigh down a rebound in CLMV tourist arrivals. As for migrant workers from CLMV, the number will likely increase this year due to arising employment opportunities in Thailand, easing quarantine rules, and a policy to systemize migrant worker management. In Thailand, the number of migrant workers from CLM has been stagnant since June 2021 at around 2.16 million, lower than its pre-pandemic reading at 2.7 million. Under such circumstances, migrant worker shortages might fuel wage rise thus deterring the performance of Thai businesses during the economic recovery.